I’m forever blowing bubbles,

Pretty bubbles in the air,

They fly so high, nearly reach the sky,

Then like my dreams they fade and die.

A song written in 1919 in the states and made famous in the music halls of Britain in the 1920’s. Football fans will instantly relate the tune to West Ham United however the song could have also been adopted by the UK press when discussing the housing market cycles.

When will it happen, how will it happen, it is bound to happen. Some pray for it (first time buyers) Some seem to bet on it on an annual basis (some members of the property press) and some are looking to take advantage of it happening (speculators / investors).

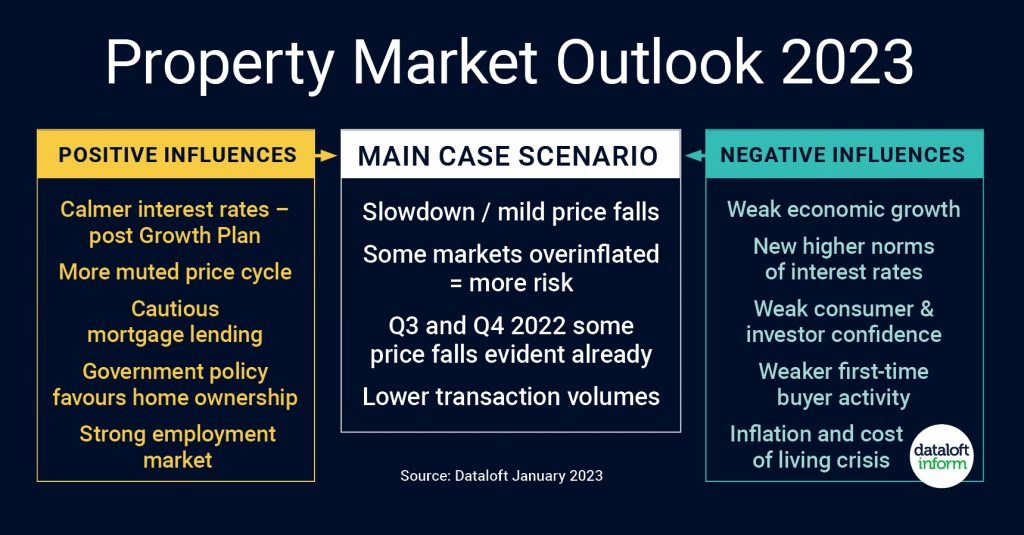

So where are we in the cycle of housing bubbles, is the bubble rising, fading or ready to burst?

Let’s look at a few fundamentals at the end of 2022:

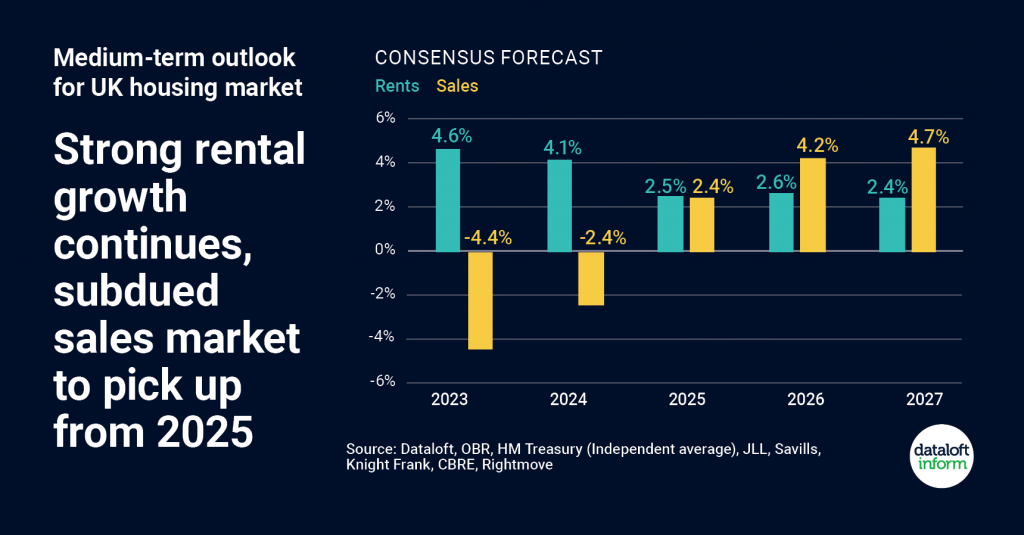

What the experts are saying – Forecasts for the next few years from Savills, Knight Frank, Rightmove

- Rental price growth is set to outpace sales price growth over the next two years. Driven by a shortage of stock and increased demand, rental growth averaging 3% per year is anticipated for the next 5 years.

- The average of the forecasts we have collated suggest UK house prices will fall by a total of -7% over the course of 2023 and 2024. At worst a fall of 10%, which is being forecast by some, will only take prices back to the summer of 2021.

- A decline in the number of homes sold in 2023 is likely, taking the annual total closer to 1 million, from 1.3 million expected this year.

- On a positive note, there is already evidence of improving affordability and choice in the mortgage markets and if this continues it should help to boost levels of buyer demand. Source: Dataloft, OBR, HM Treasury (Independent average), JLL, Savills, Knight Frank, CBRE, Rightmove, Zoopla, UK Finance

Bubble analysis = Fading. The average analysis shown in the graph over the next two years shows a decrease in prices of 6.8%. However, the individual contributors have mixed thoughts about the actual number, for example Rightmove believe the prices will decrease by only 2%, Savills by 10%, Frank Knight by 10%, JLL by 6%, the OBR by 9% proving that there is no crystal ball, just a fair, experienced judgement. What is known is that the decreases will be felt differently across the country and be specific to local markets.

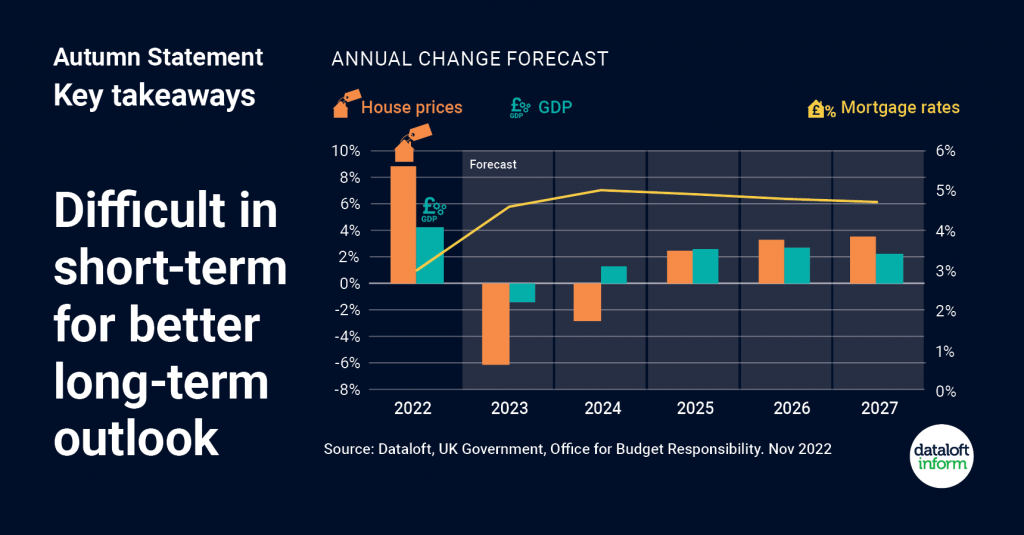

What the government are saying – The autumn statement from the Government / OBR

The Chancellor pledged to face the economic storm, as he announced widespread spending cuts and tax rises in his Autumn Statement on 17th November 2022, to tackle inflation and escalating mortgage costs.

In the short term GDP is likely to shrink by 1.4% in 2023 but then, due to the new measures being taken, is expected to grow by 9% by the end of 2027.

The expected 9% increase in house prices this year is likely to be countered by a fall over the course of 2023-24 but price growth is set to resume in 2025.

Mortgage rates are now expected to peak at 5%. The steps taken have been made to protect long-term economic growth and rebuild the UK economy, which is now officially in recession. Source: Dataloft, UK Government, Office for Budget Responsibility

Bubble analysis = Fading. The November statement delivered by Jeremy Hunt explains that the UK will go into a recession with an expected downturn in the national GDP (gross domestic product) figures. These GDP figures are historically linked to the performance of house prices where on average for every 1% decrease in GDP we will see a house price reduction of 5%.

What the lenders are doing?

- The UK’s top ten mortgage lenders lent an eye-watering £260 billion in 2021, increasing their market share to 84.4%, up from 82.4% in 2019 (data released in August 2022, UK Finance).

- The top 4 lenders retain their rankings with Lloyds Bank in first place followed by NatWest, Nationwide and Santander, with no new entrants to the Top 10 (UK Finance).

- Buy-to-Let lending accounted for 16% of all lending in 2021, no change from previous year (UK Finance).

- Of over 5,500 landlords surveyed in May 2022, only 13% expected their portfolio to decrease over the next 1–2 years. 69% anticipated no change and 18% saw it increasing (Property Academy).

Bubble analysis = Mixed. We have all seen the banks and building society mortgage rates leap. However as we enter the final few days of the year we have sen these start to reduce over the last month. Fixed rates are now available between 4.5% and 5% and tracker and discounted mortgages are becoming more popular as rates have increased. The main message is that we do not have a credit crunch where lenders are unwilling to lend.

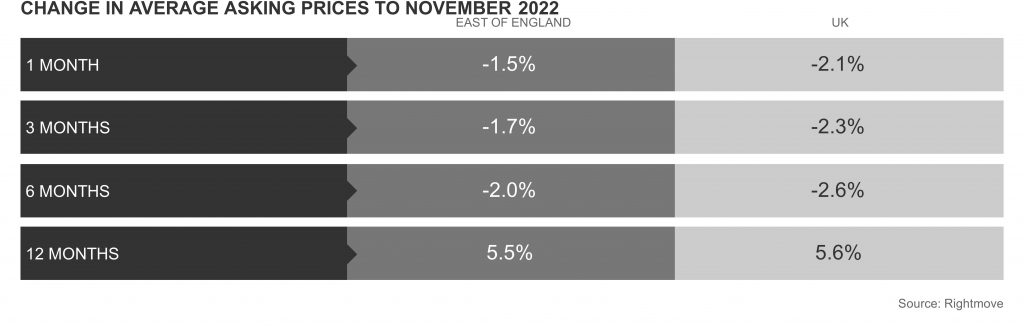

What’s been happening to asking prices?

Bubble analysis = Fading. Rightmove have seen asking prices decline for the first time in a number of years however are reporting that they only expect a 2% decline in 2023. This seems optimistic if people do want to move home.

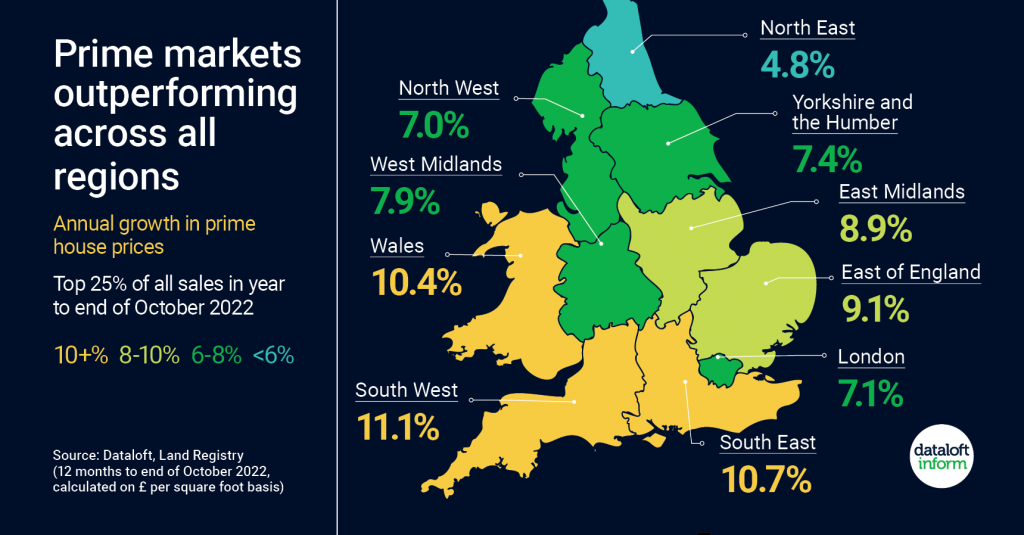

What about the prime market?

- All 10 regions across England and Wales have registered an outperformance of prime homes (top 25% of sales) in the 12 months to end of October 2022.

- This ranges from 4.8% growth in the North East to 11.1% in the South West. The average rate of annual growth for the top quartile of the market stands at 8.4%.

- Prime markets have, on average, increased 2.7% more than the market as a whole.

- Nationally, house price growth has slowed considerably overall but there will remain opportunities for growth, including in prime markets where buyers have more equity and are less reliant on mortgage finance. Source: Dataloft, Land Registry (12 months to end of October 2022, calculated on £ per square foot basis)

All 10 regions across England and Wales have registered an outperformance of prime homes (top 25% of sales) in the 12-months to end of October 2022. This ranges from 4.8% growth in the North East to 11.1% in the South West. The average rate of annual growth for the top quartile of the market stands at 8.4%. Prime markets have, on average, increased 2.7% more than the market as a whole. Nationally, house price growth has slowed considerably overall but there will remain opportunities for growth, including in prime markets where buyers have more equity and are less reliant on mortgage finance. Source: Dataloft, Land Registry (12 months to end of October 2022, calculated on £ per square foot basis)

Bubble analysis = Mixed. Prime markets will perform differently in different part of the UK. The low cost of the pound means that international buyers have benefitted in 2022 and will continue to benefit into 2023 meaning that the London Prime market should see a softer landing in this downturn. Elsewhere, the increasing cost of finance and stamp duty will mean that buyers have more choice and negotiating power than they have had in the previous 24 months. Also, due to increased house prices in the past 5 years many houses are now seen as being in the prime market meaning that this market has grown in size and choice.

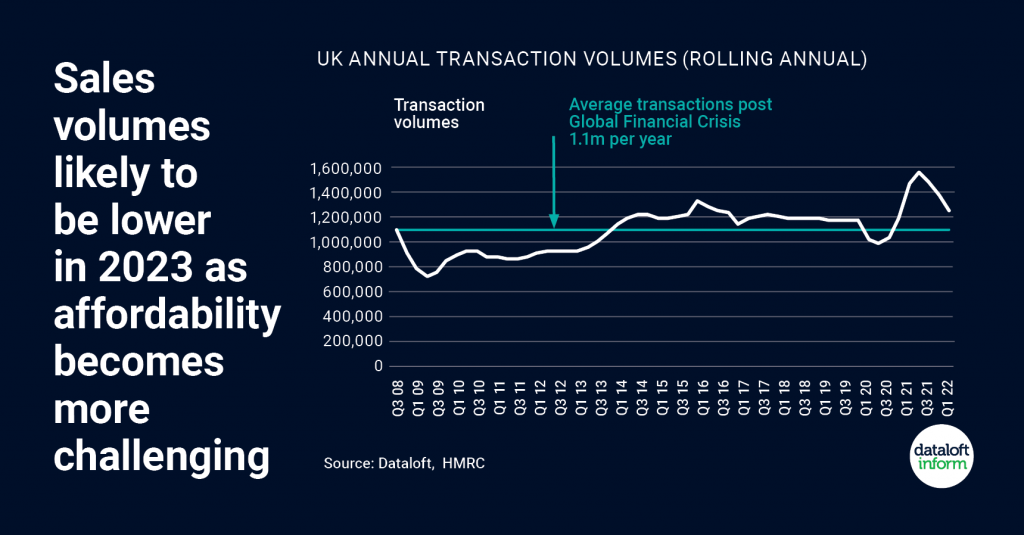

If I want to move, what choice will I have in 2023?

With rising interest rates and more challenging affordability (especially for first-time buyers), sales volumes will likely slow in 2023.

Uncertainty has an impact on housing market activity; with a new Prime Minister and Chancellor there is hope that this extra layer of uncertainty clears.

Current sales volumes are just over 1.2 million a year; a 12% fall would take them to the average level post the Global Financial Crisis.

More significant falls are possible dependent on where interest rates end up but there are some counter indications in today’s market.

Recent behavioural changes from Covid are still driving demand as movers look for more outside space and space to work from home.

Family circumstances mean there is always a core level of sales activity, plus 56% of owner occupiers have no mortgage and won’t be affected by interest rate rises. Source Dataloft, HMRC

Bubble analysis = Fading. There are different expectations on transaction levels newt year with forecasters expecting a fall of between 10% to 20%. However this does not mean that the choice of homes available will decrease. We are starting to see rising stock levels in the last quarter of 2022 which we expect to continue into the first quarter of 2023 meaning there will be more choice for buyer’s.

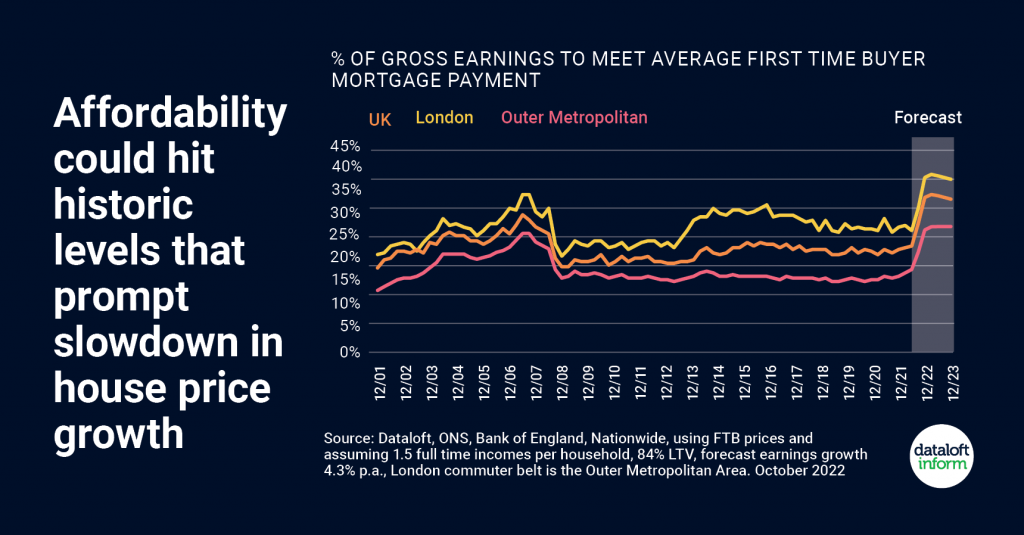

How much more expensive will it be in 2023 to buy and run a home?

- Significant rises to mortgage interest rates will mean fewer first time buyers able to get on the housing ladder. New borrowers won’t have the luxury of existing low rates.

- We tracked ‘affordability’ over the past 20 years – based on the proportion of gross income needed to meet mortgage payments. Interest rate rises drive up monthly payments.

- While it is possible that interest rates will subside if the financial markets settle, it seems unlikely and the expected rise takes affordability to levels that normally trigger a slowdown in house price growth and transactions.

- In London, the average first time buyer will need another £500 pcm if mortgage rates rise to 6% as forecast. That comes on top of a similar increase earlier this year.

- Outside the more expensive parts of the UK housing market, there may be more headroom to afford interest rate increases. Source: Dataloft, ONS, Bank of England, Nationwide

Bubble analysis = Fading. We have seen an increase of 10% in the cost of buying and running a home in 2023 which will continue to rise into the first half of 2023 with increasing costs for fuel expected in April 2023. However the longer term forecast is that this cost will fall in 2024 / 25.

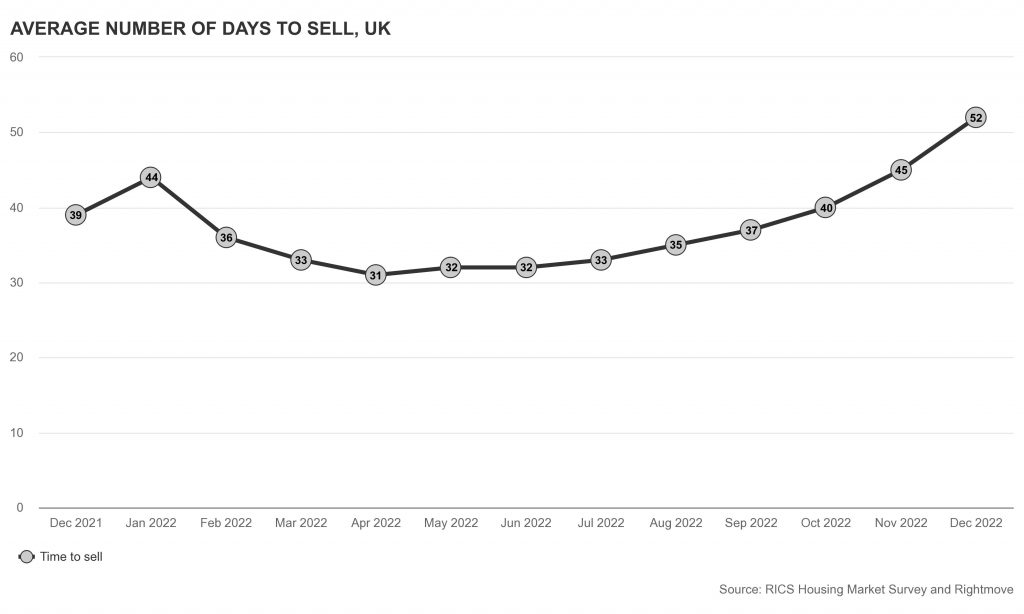

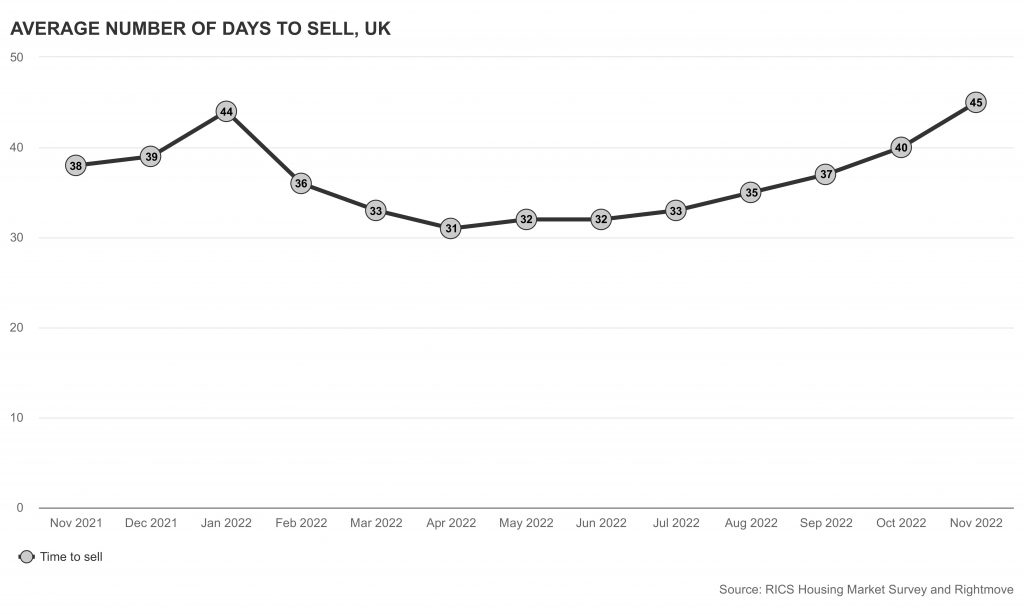

The time is takes to sell a property

Bubble analysis = Fading. The average time to sell a property nationally rose to 45 days in November from the low of 31 days in April. There is a good chance this will rise nationally to 60+ days in the first quarter of 2023.

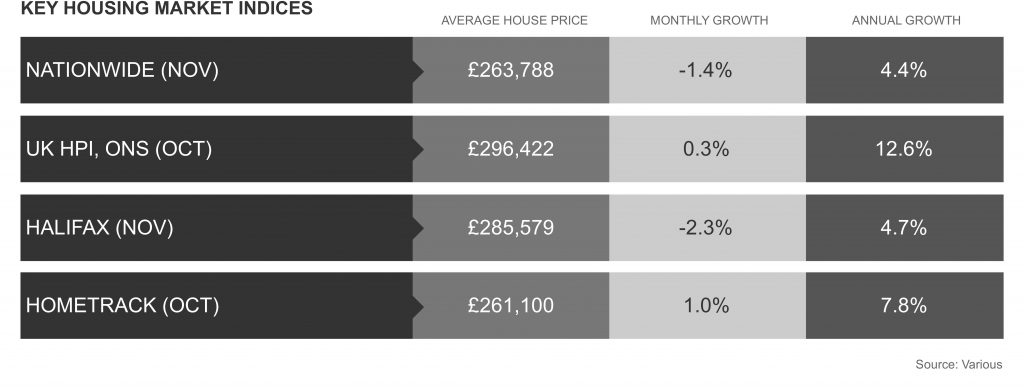

The average price of a property

Bubble analysis = Fading. The 12 month growth average for house prices has been strong. However, the most recent monthly figures are far weaker showing the turning market and weaker house prices going into 2023.

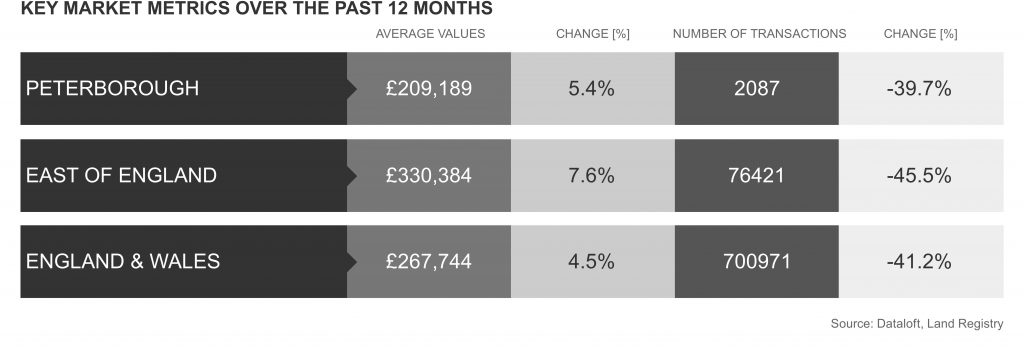

So what about our local market in Peterborough

Peterborough has seen a 27.1% rise in property prices in the last 5 years. (All Dataloft December 2022)

Peterborough has seen an average sales price rise of 5.4% during the last 12 months (England and Wales 4.5%).

Peterborough has seen a reduction of transactions of 39.7% during the last 12 months.

Peterborough has seen an average sales price of £209,189 during the last twelve months (England and Wales £267,744).

Only 13.4% of transactions in Peterborough were flats during the last twelve months.

Bubble analysis = Mixed. We are experiencing local reductions in property prices in the last quarter of 2023 as well as a decreasing demand from buyers. The average daily views per property for Peterborough in December is currently 45 view per day (Tortoise Property 100.3 views per day). In May 2022 we experienced average daily viewing figures of 99.5 view per day in Peterborough (Tortoise Property 332.4 views per day) which highlights the difference in demand. Also there has been 5758 sales instructions in the Greater Peterborough area this year with 3176 agreed sales. The expectation is that the agreed sales figures will reduce by 15%+ in 2023 meaning we move back to a more balanced market place where marketing and attracting the correct buyer will be important to owners that are looking to sell.

Peterborough enjoys many advantages to other City’s in the UK, being one of the top 10 City’s for growth, however we are susceptible to high rises in living costs due to our lower average salary levels and disposable income figures compared to some parts of the UK. We are though attractive to buyers moving northwards where access to London and its suburbs are required for work and to visit family. In 2022 alone first time buyers leaving London spent £8.35 billion pounds on property. Up to date data can be found on our Market Data page on our website https://www.tortoiseproperty.co.uk/market-data.html

Our bubble summary:

Nationally we looked at 9 areas that overall see the house prices fading into 2023. We expect the Bank of England interest rate to settle around 4% to 4.25% in the New Year due to a more controlled approach from the government. The inflation costs however for consumers (including housing) stands at 9.3% which is affecting buyers ability to buy and run new homes. With these two numbers contributing to the costs of living crises will mean that we see a reduction in GDP which ultimately effects the cost of home. Expect house prices therefore to fade rather than crash through 2023 / 24.

In Peterborough the increase in house prices has been influenced by the decrease in transactions over the previous twelves months whilst experiencing a high demand from buyers into the start of September. This has now changed with a normal number of buyers with choice going into 2023.

We continue to blow bubbles here at Tortoise Property and check to see if they are on the rise, when they seem to fade and give some pointers where possible as to when they may burst!

So until the next time….

Fortune’s always hiding,

I’ve looked everywhere,

I’m forever blowing bubbles,

Pretty bubbles in the air.

Mike Matthews

Tortoise Property